Blog

Retirement Spending Is Not Linear: Plan for the Phases

Retirement Spending Is Not Linear. It’s Phase-Based.

Most retirement plans assume spending will remain steady year after year.

In reality, retirement spending typically follows phases. It often peaks in the early years of retirement, declines in mid-retirement, and changes again later depending on health, lifestyle, and priorities.

At Harmony, we intentionally plan for this pattern. Our annual review process focuses not just on what happened last year, but on forward-looking income and spending strategy based on life stage.

Why Traditional Retirement Projections Miss the Mark

Many retirement calculators assume:

Spending remains flat

Inflation increases expenses gradually

Lifestyle remains consistent

However, research and real-world experience show spending is “lumpy” and staggered.

Spending often:

Increases in your 50s and early retirement years

Peaks around early retirement due to travel and lifestyle spending

Gradually declines in your 70s

Shifts toward healthcare in later years

Planning as if every year is identical creates risk.

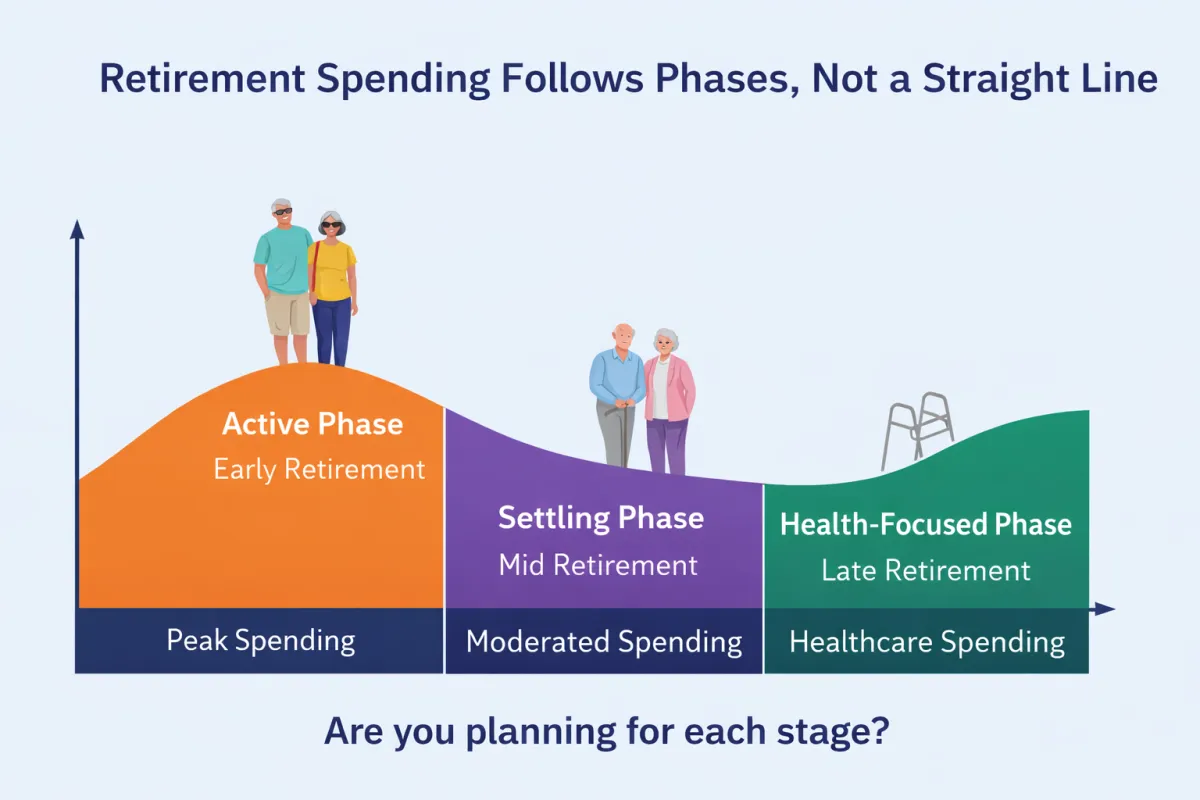

The Three Phases of Retirement Spending

1. The Active Phase (Early Retirement)

Typically ages 60–70.

Spending is often highest during this stage because:

Health is still strong

Travel and lifestyle goals are pursued

Major experiences are prioritized

This is when retirees often enjoy the lifestyle they worked decades to build.

2. The Settling Phase (Mid Retirement)

Typically ages 70–80.

Spending generally stabilizes.

Travel slows down

Major purchases decrease

Lifestyle becomes more routine

Expenses are often lower than the early retirement years.

3. The Health-Focused Phase (Late Retirement)

Typically, 80+.

Spending patterns shift again.

Healthcare expenses may increase

Mobility decreases

Lifestyle spending reduces significantly

The nature of expenses changes even if total spending declines.

Why Does This Matters for Financial Planning?

If you assume spending is flat, you may:

Over-save and underspend in your healthiest years

Or under-plan for late-life healthcare needs

The objective is not simply preserving capital.

The objective is aligning wealth with life stage.

A larger portfolio later in life does not necessarily increase satisfaction if health limits lifestyle.

Spend When You Can Enjoy It

Data consistently shows that spending peaks in the 50s and early retirement years.

Health and energy are typically strongest then.

At Harmony, we believe financial planning should recognize this reality.

Your net worth does not need to peak at the very end of life.

It may be more rational for wealth to support higher spending in earlier retirement, while you can fully enjoy it.

Memories and experiences should not be deferred indefinitely.

Harmony’s Phase-Based Planning Approach

At our annual review meetings, we do not only evaluate performance.

We also review:

Future income planning

Expected lifestyle changes

Phase-based spending adjustments

Withdrawal sequencing strategy

Healthcare planning assumptions

Retirement is dynamic.

Your plan should be dynamic as well.

Rather than relying on a single linear projection, we evaluate multiple spending paths across different life stages.

This allows clients to spend confidently in earlier retirement years without fear of prematurely exhausting assets.

Frequently Asked Questions

Does retirement spending always decrease with age?

Not always. It often peaks early in retirement, declines in mid-retirement, and may increase again due to healthcare costs.

Should retirees spend more in their early retirement years?

If financially sustainable, it often makes sense to allocate more spending to years when health and mobility are strongest.

Why do traditional retirement plans assume linear spending?

Linear assumptions simplify projections. However, they do not always reflect real human behavior.

How does Harmony plan for phase-based spending?

We incorporate life-stage projections into annual reviews and adjust income planning accordingly. Our focus is forward-looking, not just performance review.

Final Thought

Retirement is not a straight line.

It is a series of phases.

Financial planning should reflect that reality.

If your retirement plan assumes every year looks the same, it may be time to revisit your assumptions.

This email is provided by Harmony Financial Solutions Inc. for informational and educational purposes only and does not constitute investment, financial, tax, legal, or insurance advice. It has been prepared without regard to your individual objectives, financial situation, or needs. Any views expressed are opinions as of the date of publication and are subject to change without notice; forward-looking statements are not guarantees of future results. Information is drawn from sources believed to be reliable but is not guaranteed for accuracy or completeness. Before acting, consider the appropriateness of any information for your circumstances and consult a qualified advisor, and where relevant a tax or legal professional. Past performance is no guarantee of future results. All investments involve risk, including the possible loss of principal.